Buying your first home is a big milestone. It’s exciting, a little overwhelming, and often filled with questions. Where do you start? How much can you afford? What steps actually matter?

The truth is, the home-buying process doesn’t have to feel complicated. When you break it down into clear steps and understand what to expect, it becomes much more manageable.

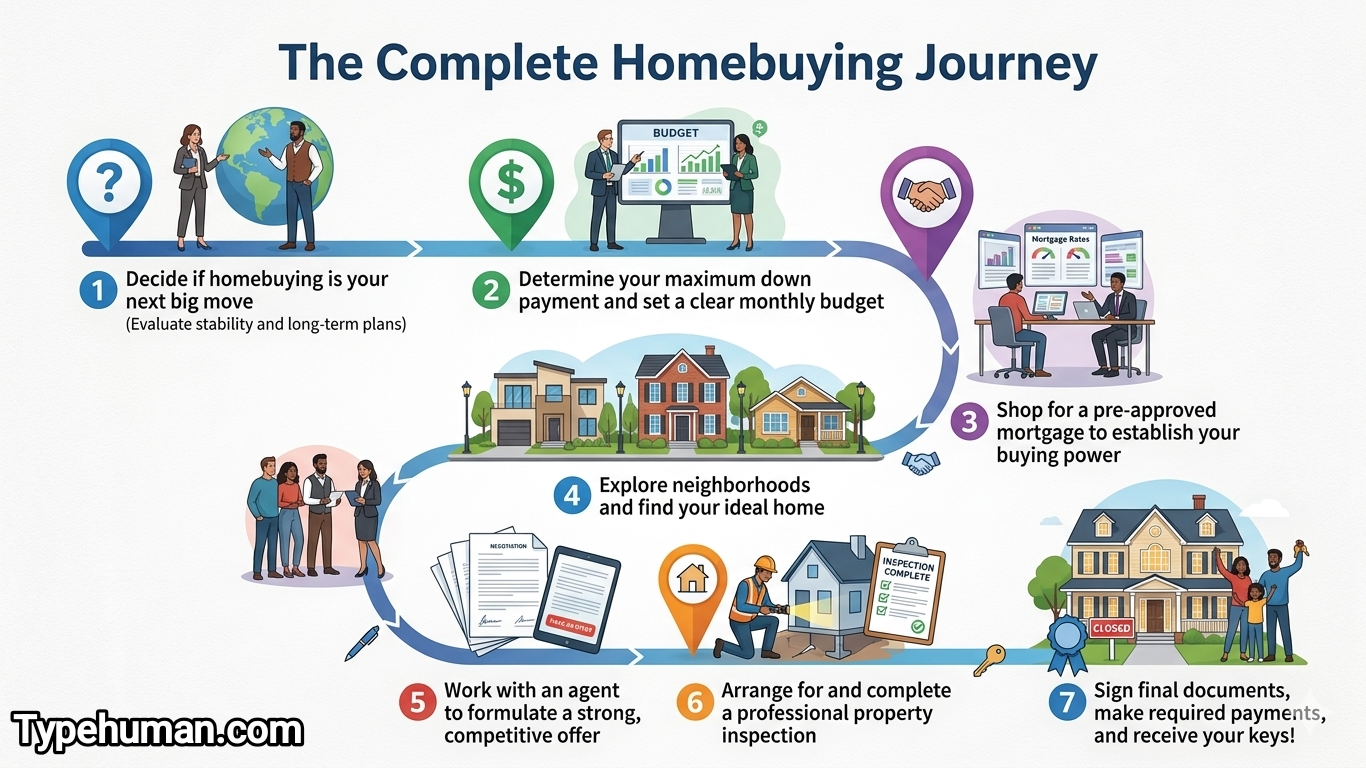

Let’s walk through how first-time buyers can confidently navigate the journey—from early planning to finally getting the keys.

Start With a Clear Financial Picture

Before looking at properties, the most important step is understanding your finances.

This means taking a close look at your income, savings, and regular expenses. It helps you figure out how much you can realistically afford without stretching yourself too thin.

For example, think about your monthly budget:

- How much do you earn?

- What are your fixed expenses (rent, bills, subscriptions)?

- How much can you comfortably set aside for repayments?

This step is similar to planning any major purchase, such as buying a car or starting a business. Knowing your limits helps you make smarter decisions.

You’ll also need to save for a deposit. This is the upfront amount you contribute toward the property. A larger deposit can reduce your loan amount and may give you access to better loan options.

Understanding the basics of a mortgage loan—how borrowing and repayments work—can also give you more confidence as you move forward.

Get Pre-Approval Before You Start Searching

Once you have a good idea of your finances, the next step is getting pre-approval for a home loan.

Pre-approval is when a lender assesses your financial situation and gives you an estimate of how much you can borrow. It’s not a final approval, but it gives you a clear price range to work with.

For example, if you’re pre-approved for a certain amount, you can focus your property search within that range instead of guessing.

This step has a few key benefits:

- It helps you set realistic expectations.

- It shows sellers that you’re a serious buyer.

- It speeds up the process when you’re ready to make an offer.

Think of it like setting a budget before going shopping. It keeps you focused and prevents unnecessary stress later on.

Finding the Right Property for Your Needs

With your budget in mind, you can start searching for a home.

This is often the most exciting part, but it’s also important to stay practical. It’s easy to get carried away by features or appearances, so try to focus on what truly matters for your lifestyle.

Ask yourself:

- Is the location convenient for work or daily activities?

- Does the layout suit your current and future needs?

- Are there nearby amenities like schools, shops, or transport?

For example, a young professional might prioritize proximity to work and public transport, while a family may focus on space and access to schools.

It’s also helpful to attend inspections and compare different properties. This gives you a better sense of value and helps you make informed decisions.

Making an Offer and Moving Forward

Once you find the right property, the next step is making an offer.

This can feel like a big moment, but it’s simply part of the process. Your offer is based on your budget, the property’s value, and current market conditions.

If your offer is accepted, the process moves into the legal and financial stages. This includes:

- Finalizing your home loan

- Conducting inspections (such as building and pest checks)

- Reviewing contracts with a professional

Midway through this stage, many first-time buyers look for guidance on financing options and requirements through resources like how to buy your first home in Australia to better understand what’s involved and ensure they’re making informed decisions.

Having the right support during this phase can make a big difference, especially when dealing with paperwork and timelines.

Understanding Settlement and Final Steps

After everything is approved, the final step is settlement.

Settlement is when ownership of the property is officially transferred to you. This is also when your loan is finalized, and funds are transferred.

For example, once the settlement is complete:

- You receive the keys to your home.

- The property is legally yours.

- Your mortgage repayments begin.

This stage can take several weeks, depending on the agreement. While it may feel like a waiting period, it’s an important part of ensuring everything is completed correctly.

Common Challenges and How to Handle Them

It’s normal to face a few challenges along the way, especially as a first-time buyer.

Some common ones include:

Feeling Overwhelmed

There’s a lot of information to take in. Breaking the process into steps helps make it more manageable.

Budget Pressure

It’s tempting to stretch your budget, but staying within your limits ensures long-term financial stability.

Decision Fatigue

Looking at multiple properties can be tiring. Focus on your priorities to make decisions easier.

For example, just like choosing a major investment or starting a new project, taking your time and staying informed helps you avoid costly mistakes.

A Journey Worth Taking

Buying your first home is a journey filled with learning, planning, and decision-making. While it may seem complex at first, each step brings you closer to a place you can call your own.

By understanding your finances, getting pre-approval, choosing the right property, and navigating the process carefully, you can move forward with confidence.

It’s not about rushing—it’s about making informed choices that support your future.

In the end, owning a home is more than just a financial decision. It’s about creating a space where you can build memories, grow, and feel secure.

And with the right approach, the process becomes not just manageable—but truly rewarding.